Key Takeaways

- When you outsource accounting services, you can gain benefits like cost savings and greater access to industry expertise, but it’s important to be aware of challenges like forming a long-term partnership and ensuring candidates understand US GAAP.

- You can outsource a wide range of accounting services, from payroll and bookkeeping to financial planning and analysis.

- Building long-term relationships with outsourced professionals and strategically selecting services to keep in-house are best practices for enhancing the effectiveness of outsourced accounting.

Maintaining accurate and efficient accounting operations is more critical than ever. Outsourced accounting has emerged as a strategic solution for companies seeking to streamline their financial processes, reduce costs, and focus on core business activities.

This article examines the pros and cons of outsourcing accounting services and explores some of the top firms to consider for your needs.

Given the success many businesses have had with outsourced accounting in recent years, leveraging these solutions with trusted partners can transform your financial management.

What Accounting Services Can You Outsource?

Outsourcing accounting services can be a game-changer, no matter what role you choose to outsource. Here’s a comprehensive look at the core accounting services you can outsource:

- Bookkeeping: This service is at the heart of any accounting system. Bookkeeping involves recording and organizing financial transactions.

- Payroll management: Managing payroll is more than just issuing paychecks. It includes calculating wages, withholding taxes, complying with employment laws, and issuing year-end tax forms.

- Accounts payable/receivable: Keep your cash flow steady by outsourcing accounts payable and accounts receivable functions. This service entails managing invoices, ensuring timely payments, and handling collections.

- Financial reporting: Accurate and timely financial reports are crucial for making informed business decisions. Outsourcing financial reporting provides professional-grade income statements, balance sheets, and cash flow statements.

- Tax services: By outsourcing tax compliance and preparation, you gain access to accounting experts who can handle everything from tax filing to strategizing for tax efficiency.

- Financial planning and analysis: Beyond just crunching numbers, outsourced accounting providers can offer insights through financial analysis and help you develop strategies for business growth and efficiency.

Should You Outsource Your Accounting?

Below, we list some benefits and potential challenges of accounting outsourcing and provide valuable insights into whether it could be the right choice for your business.

Pros of outsourcing accounting services

Outsourcing your accounting services provides numerous benefits, including:

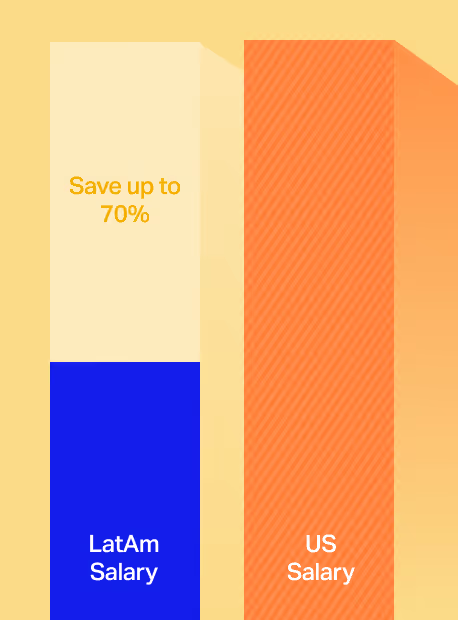

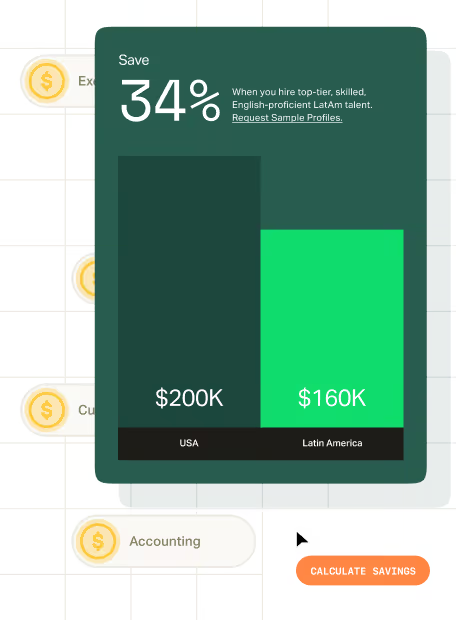

- Lower salary costs: One of the main advantages of outsourcing financial services is that you can often find accounting talent in regions where labor expenses are lower than in the US. For example, Latin America (LatAm) is a popular outsourcing destination due to its pool of highly skilled remote professionals with lower salary expectations than their US counterparts.

- Flexible hiring arrangements: Outsourcing also offers flexibility in terms of the level of support you require. For instance, you can hire per hour and get support as and when you need it rather than having to pay for a full-time employee who may not always be required. This can be a particularly cost-effective solution for smaller businesses.

- Industry expertise: Outsourced accounting allows you to find talent that has worked for companies or clients in similar industries and understands your specific accounting requirements. This can be particularly useful for businesses with complex accounting needs operating in niche industries.

- Advanced knowledge of accounting tools: Outsourcing can open up your options for working with talent that has advanced knowledge of accounting tools such as QuickBooks, NetSuite, or SAP, which can save you the time and effort of teaching these tools to an in-house accounting team.

- Global talent pool: Accounting outsourcing gives you access to a far larger pool of accounting talent. You can easily expand your search to find accounting professionals worldwide, providing you with a wider range of skill sets and experiences to choose from.

Cons of outsourcing accounting services

It’s also critical to be aware of potential accounting outsourcing challenges, such as:

- Limited knowledge of US GAAP: Not all talented accounting professionals from outside the US will understand the US Generally Accepted Accounting Principles (GAAP). If compliance with US GAAP is essential for your business, make sure you check whether candidates have the required knowledge.

- Challenges in forming a long-term partnership: Depending on the outsourcing provider you select, your outsourced accounting team may feel more like suppliers than team members without the daily interactions that come with working in-house. In our tips below, we discuss why it’s important to put in extra effort to build a long-term bond with outsourced accounting professionals.

Alternatives to Traditional Outsourcing: Building Your Own Offshore Accounting Team

Instead of outsourcing accounting functions to a third-party service provider, many companies are choosing to hire their own remote accounting professionals.

This approach gives you more control over your team while still accessing global talent at competitive rates.

When you hire your own remote accounting team members, you maintain direct oversight, ensure better cultural integration, and build long-term relationships that benefit your business.

According to Near's State of LatAm Hiring Report, companies save on average 55% by hiring accountants in Latin America compared to in the US.

This is where specialized recruiting and staffing companies like Near come in, helping you build your own remote accounting team rather than outsourcing the function entirely.

Top 5 Outsourced Accounting Firms

Below, we’ve compiled a list of top accounting firms known for their expertise in providing outsourced services.

This list includes companies that specialize solely in accounting solutions and those that incorporate these services within their broader offerings. Please note that the firms are not listed in any specific order.

1. Near

Near (Hire With Near) is a full-service staffing and recruiting agency that helps US companies of all sizes hire top-performing remote talent in Latin America across finance, accounting, sales, software engineering, AI, data, design, marketing, operations, and virtual assistance.

We've built our entire process around helping you find professionals who'll become true members of your team. Our done-for-you hiring process means you typically receive candidate lists within 3 days and complete placements in under 3 weeks.

- No upfront costs: With Near, you never pay anything upfront. Once you make a hire, you can choose between a one-off fee and a monthly fee, depending on whether you prefer us to handle payroll and compliance

- Pre-vetted talent pool: We have over 45,000 candidates, but we don't just search there. We find you talent that meets your exact requirements and expectations, including many with Big Four experience

- Real-time collaboration: By hiring LatAm talent, you get seamless communication from close time zones without sacrificing quality or cultural alignment

Just ask CyberFortress, a rapidly growing cybersecurity company that hired an entire 20-person accounting team through Near, saving an estimated $1.2M annually while actually improving their operations, cutting their month-end closing timeline from 15 days to 10 days.

2. Moss Adams

Moss Adams is an accounting, consulting, and wealth management solution boasting 111 years in business. It caters to clients across all 50 states from over 30 locations in the Western US and beyond.

3. Baker Tilly

Born out of Depression-era Waterloo, Wisconsin, Baker Tilly has risen from humble beginnings to provide advisory series to a myriad of industries. Its cloud alliances include ADP, Bill, Expensify, Intuit QuickBooks, and Sage.

4. AccountingDepartment.com

The nationwide accounting service AccountingDepartment.com has over two decades of experience handling accounting tasks for US businesses.

The company offers a comprehensive range of accounting services, including everything from financial reporting, bookkeeping, and payroll processing to consulting and tax preparation.

5. Deloitte

As a Big Four accounting firm, Deloitte is a global leader in accounting and finance services. It can handle CFO advisory, auditing, financial consulting, tax advisory, and much more.

With its vast presence and expertise in international standards, Deloitte can be an excellent outsourcing partner for US businesses.

5 Important Tips When Outsourcing Accounting Services

Outsourcing accounting services can be a smart business move for many companies. However, it’s imperative to approach this choice with careful consideration and strategic planning. Here are some tips to keep in mind:

1. Secure your accounting information online

One of the best ways to secure your accounting information online is to use cloud storage or migrate to a cloud-based accounting system. This technology allows you to keep all accounting records, reports, statements, and other sensitive financial data on a secure server that can only be accessed with a login and password.

This will make the backup process easier, and your accounting data will always be safe and accessible in case of system failures or other disasters. Moreover, if you’re working with a remote team or are outsourcing to a provider in a different location, a cloud system will make it easier for them to access the data they need.

2. Use accounting management software

Using accounting management software can help you keep track of your financial records, simplify the accounting process considerably, and save you valuable time and money in the long run. Outsourcing your accounting services also provides benefits like the following:

- Streamlining processes: Using software to streamline processes such as bookkeeping, billing, and financial reporting makes it easier for outsourced accounting service providers to manage financial data. It also reduces the potential for accounting errors.

- Data security: Given that almost all data breaches are motivated by financial gain, outsourcing accounting services can increase the risk of data breaches or theft. However, accounting software can provide additional layers of security, such as encryption and user authentication, to protect sensitive financial information.

- Cost effectiveness: Accounting management software reduces the need for manual labor, reducing the hours the outsourced team has to put in.

- Improved communication: Real-time access to financial data can enable better collaboration and informed decision-making, leading to improved financial performance.

- Scalability: Most accounting management software can easily scale up or down to accommodate changes in business size and accounting needs. This flexibility benefits particularly fast-growing companies or those undergoing significant changes.

3. Build long-term relationships with outsourced accounting professionals

Hiring a new accounting team every time you lose one can be expensive and time-consuming. Developing a long-term relationship will help avoid these turnover costs. You won’t have to spend time and resources training new accounting teams on your company’s accounting procedures and business processes.

A long-term partnership with your outsourced accounting team gives them the time to become familiar with your business and understand your unique accounting needs. As a result, they will be able to tailor their services to better satisfy those needs and even spot trends and potential issues easier, saving you both time and money.

4. Separate treasury from accounting

When outsourcing treasury functions to a third party, you may expose your company’s financial information to potential security risks.

By keeping the treasury in-house and allowing access only to the most trusted team members, you can maintain the financial security and confidentiality of your organization and reduce the risk of data breaches, financial mistakes, and fraud or embezzlement.

5. Don’t outsource invoicing

Outsourcing invoicing to an accounting firm can be more expensive than necessary, and it may not add much value to your business.

While invoicing is related to accounting, it is not strictly an accounting function. It’s a relatively simple process that does not require specialized accounting knowledge; therefore, it can be handled by most business owners or administrative staff.

{{state-latam-hiring}}

Final Thoughts

Here's what we've learned from working with hundreds of companies on their accounting hiring: the best talent isn't limited by geography.

The companies seeing the biggest wins aren't just cutting costs. They're accessing talent they couldn't find locally. We're talking about senior accountants with Big Four experience, controllers who can streamline your month-end close, and financial analysts who bring fresh perspectives to your business challenges.

The choice between traditional outsourcing and building your own remote team comes down to control.

When you hire your own people, they learn your business, understand your goals, and stick around longer. According to our data, companies retain remote LatAm hires 66% longer than US-based employees.

Companies like CyberFortress didn't just save $1.2M annually. They actually improved their operations, cutting their closing process by five days. That's the difference between treating accounting as a cost center versus building it as a competitive advantage.

The opportunity is there if you're ready to think beyond traditional hiring boundaries. You could access senior-level expertise, cut your hiring timeline from months to weeks, and free up budget for other growth initiatives.

Ready to see what's possible? Get a list of pre-vetted accounting candidates you can interview for free. You won't pay anything unless you make a hire.

.avif)

%20(1).avif)

%20(1).png)